December 29, 2009, 4:40 pm

Terrorism priorities

テロリズムの優先順位

A number of people — though not, strange to say, any leading figures in the Democratic party — have pointed out that the TSA doesn’t have an administrator at the moment, because Sen. Jim DeMint is holding up Obama’s nominee. Why? Because DeMint is worried that TSA employees might unionize.

多くのヒトが、妙な話だが、民主党内の指導者だけでなく、TSA(アメリカ国土安全保障省)は、テロの時に管理者不在であったと指摘している。 ジム・デミット共和党議員は、オバマ推薦の行政官を拒否しているからだ。なぜかって? TSA労働者が結成することを不安視しているからだ。

So much for making the fight against terror a priority. But then, it has been this way from the start. Whenever I hear someone talk about how we were unified as a nation after 9/11, I gag — partly because I remember how senior Republicans tried to keep airport security in private hands. Just weeks after the attack, preventing any expansion of government was more important to them than protecting passengers.

テロに対する戦いを優先にするには、色々と準備が必要だ。しかし、それなら最初からそうするようにしておかならければいけない。 9/11以降に1人の国家として、我々がいかに1つになったかを誰かが話すとき、常に息が詰まる。 共和党の上院が、どのように民間に空港のセキュリティを維持しようとしていたか記憶している。 そのテロの後、数週間で、政府の拡大を防ぐことが、乗客を守るより重要になっていた。

Nothing has changed.

何も変わっていない。

1229 Yes, we have no bananas

December 29, 2009, 8:10 am

Yes, we have no bananas

もうバナナ戦争はない。

The banana wars are over. And at a personal level I’m sorry to see them go.

バナナ戦争は既に終戦している。個人敵には、終戦には残念に思っている。

バナナ戦争とは、第一次世界大戦後にアメリカ合衆国によって行われた中央アメリカ諸国に対する軍事介入の総称。

You see, ever since the third edition of the world’s leading textbook in international economics, we’ve had a box on bananas titled “Do trade preferences have appeal?” The original box ended by saying,

At the time of writing, effort to negotiate a resolution to Europe's banana split had proved fruiteless.

というのは、世界経済学の第1級の教科書の第3版以来、私は、”Do trade preferences have appeal?" と題したバナナに関する囲みコラムを掲載してきたからだ。このコラムの原本では、この執筆時点では、ヨーロッパのバナナ問題の解決に向けた交渉の努力は、実りないものに終わっている。という文句で締められている。

But ninth edition (with Marc Melitz on board) will have to be debananified. Darn.

しかし、第9版では、もうバナナ抜きになってしまった・・・あーあー。

Yes, we have no bananas

もうバナナ戦争はない。

The banana wars are over. And at a personal level I’m sorry to see them go.

バナナ戦争は既に終戦している。個人敵には、終戦には残念に思っている。

バナナ戦争とは、第一次世界大戦後にアメリカ合衆国によって行われた中央アメリカ諸国に対する軍事介入の総称。

You see, ever since the third edition of the world’s leading textbook in international economics, we’ve had a box on bananas titled “Do trade preferences have appeal?” The original box ended by saying,

At the time of writing, effort to negotiate a resolution to Europe's banana split had proved fruiteless.

というのは、世界経済学の第1級の教科書の第3版以来、私は、”Do trade preferences have appeal?" と題したバナナに関する囲みコラムを掲載してきたからだ。このコラムの原本では、この執筆時点では、ヨーロッパのバナナ問題の解決に向けた交渉の努力は、実りないものに終わっている。という文句で締められている。

But ninth edition (with Marc Melitz on board) will have to be debananified. Darn.

しかし、第9版では、もうバナナ抜きになってしまった・・・あーあー。

1229 Fannie, Freddie, and full faith

December 29, 2009, 8:27 am

Fannie, Freddie, and full faith

ファニー、フレディ、フルフェイス

I don’t exactly disagree with what Tim Duy, Calculated Risk, and Dean Baker are saying about the decision to explicitly back Fannie and Freddie. But I think it adds to our understanding if you think of Fannie and Freddie as being, in effect, in the same business as the Fed these days.

Tim Duy's Fed Watch(有名なブログ)、Calculated Risk、ディエン・ベーカーが言うようなファニィーやフレディを明示的に支援する主張には、はっきりとは同意できない。ただ、ファニーやフレディが、最近のFedのような役割において有効に機能すると考えるのであれば、我々の理解を深める助けになるだろう。

That is, if you think about what the Fed is doing when it engages in “quantitative easing” — expanding its balance sheet by buying unconventional assets — you realize that it’s part of a broader provision of credit to the private sector by governmental or quasi-governmental agencies, which are ultimately financed or at least backstopped by public debt.

それは、Fedが”量的緩和”に従事する際にするべきこと、とんでもない資産を買って負債を拡大させること(皮肉) を考えると、政府や準政府機関(最終的に資金供与する、少なくとも公共負債によって助ける機関)による民間部門へのある種の広い範囲で信用供与になる。と理解して頂けるだろう。

Why do this? Part of what depressed the economy during the financial crisis was a widening spread between government debt and private borrowing costs — not just in things like the TED spread, but also in mortgage rates:

なぜ、こんなことをする必要があるのか? それは、金融危機により政府の貸付けと民間の借入れコストの差が拡大している間、この種のことが経済を落ち込ませていた。(これはTED(T-bill とEuroDallorの金利差)の拡大のようなことだけではなく、住宅ローンにも当てはまる)

This spread was narrowed thanks to a combination of Fed actions and the expansion of Fannie-Freddie lending.

この金利差は、Fedの介入とファニーやフレディの融資拡大が合わさったお陰で、縮小した。

And the administration very much wants to keep this kind of intervention going. You can argue that some other policy — inflation targeting by the Fed, expanded fiscal stimulus, whatever — would be better. But none of these things seem politically possible. Keeping Fannie and Freddie fully engaged in the mortgage-support business is one of the few tools available to prop up a still very weak economy. And so they’re doing it.

そして、政権は、この種の介入を引き続き求めている。Fedによるインフレターゲットや、財政出動、などより素晴らしい策があったかもしれないが、政策的にはこれらのことは難しかった。ファニーやフレディを住宅ローンサポートに従事させることは、未だに弱い経済を下支えするのに有効な数少ない手段の1つである。

Fannie, Freddie, and full faith

ファニー、フレディ、フルフェイス

I don’t exactly disagree with what Tim Duy, Calculated Risk, and Dean Baker are saying about the decision to explicitly back Fannie and Freddie. But I think it adds to our understanding if you think of Fannie and Freddie as being, in effect, in the same business as the Fed these days.

Tim Duy's Fed Watch(有名なブログ)、Calculated Risk、ディエン・ベーカーが言うようなファニィーやフレディを明示的に支援する主張には、はっきりとは同意できない。ただ、ファニーやフレディが、最近のFedのような役割において有効に機能すると考えるのであれば、我々の理解を深める助けになるだろう。

That is, if you think about what the Fed is doing when it engages in “quantitative easing” — expanding its balance sheet by buying unconventional assets — you realize that it’s part of a broader provision of credit to the private sector by governmental or quasi-governmental agencies, which are ultimately financed or at least backstopped by public debt.

それは、Fedが”量的緩和”に従事する際にするべきこと、とんでもない資産を買って負債を拡大させること(皮肉) を考えると、政府や準政府機関(最終的に資金供与する、少なくとも公共負債によって助ける機関)による民間部門へのある種の広い範囲で信用供与になる。と理解して頂けるだろう。

Why do this? Part of what depressed the economy during the financial crisis was a widening spread between government debt and private borrowing costs — not just in things like the TED spread, but also in mortgage rates:

なぜ、こんなことをする必要があるのか? それは、金融危機により政府の貸付けと民間の借入れコストの差が拡大している間、この種のことが経済を落ち込ませていた。(これはTED(T-bill とEuroDallorの金利差)の拡大のようなことだけではなく、住宅ローンにも当てはまる)

This spread was narrowed thanks to a combination of Fed actions and the expansion of Fannie-Freddie lending.

この金利差は、Fedの介入とファニーやフレディの融資拡大が合わさったお陰で、縮小した。

And the administration very much wants to keep this kind of intervention going. You can argue that some other policy — inflation targeting by the Fed, expanded fiscal stimulus, whatever — would be better. But none of these things seem politically possible. Keeping Fannie and Freddie fully engaged in the mortgage-support business is one of the few tools available to prop up a still very weak economy. And so they’re doing it.

そして、政権は、この種の介入を引き続き求めている。Fedによるインフレターゲットや、財政出動、などより素晴らしい策があったかもしれないが、政策的にはこれらのことは難しかった。ファニーやフレディを住宅ローンサポートに従事させることは、未だに弱い経済を下支えするのに有効な数少ない手段の1つである。

1228 Renminbi RX

December 28, 2009, 12:16 pm

Renminbi RX

中国人民元(RMB = RenminBi 人民幣) RX = EP*/P

Dean Baker is right: it’s bizarre to report that Chinese officials are (a) worried about inflation and (b) determined not to let their currency appreciate without noting that these are contradictory policies.

このリンク先でのディーン・ベイカーの主張は、正しいよ。中国高官はインフレに怯えて、これらは矛盾した政策以外何物でもないのに人民元切り上げを実施しようとしない。

Consider the real exchange rate, defined as RX = EP*/P, where E is the exchange rate measured as the domestic currency price of foreign currency (so an appreciation of the renminbi is a fall in E), P* is the foreign price level, and P the domestic price level. Basic international macro says that there is a “natural” level of the real exchange rate, determined by trade competitiveness and international capital flows. And the economy “wants” to get to that real exchange rate.

為替レートを考慮すると、RX = EP*/Pと定義される。

Eは、国内通貨の海外通貨での価値(人民元の切り上げは、Eの下落になる)

P*は、外国の物価水準

Pは、国内の物価水準

基本的な国際マクロ経済学では、実質為替レートには、市場競争力や国際的な資本の流れによって、適切な水準がある。 経済は、実質為替レートに近づこうとする。

If you have a floating exchange rate, you get there via a rise or fall in E. But if you have a pegged rate, there’s pressure on prices instead. By deliberately keeping E higher than it would be under floating, China is creating pressures for P to rise; the inflationary pressures are directly related to the exchange rate policy.

変動為替相場を採用しているのであれば、E(国内通貨の海外通貨での価値)の上下によって価格が形成される。しかし、固定為替相場であるなら、故意にEを高くすることによって価格に圧力を与えることになる。中国では、P(国内の物価水準)が上がるのを抑えるために価格形成をしている。 つまり、インフレ圧力は、直接為替政策に関係している。

This isn’t a new story. The proximate cause of the breakup ofBretton Woods [actually not quite: it was the Smithsonian Agreement, the short-lived successor to Bretton Woods, that broke up and ushered in floating rates] was the fact that Germany, whose currency was pegged to the dollar, found itself facing inflationary pressures; the Germans solved that problem by letting the Deutsche mark float, and the rest is history.

過去にも事例がある。最も最近の例では、ブレトンウッズ体制の崩壊を引き起こしている。

(正確には、そうではない。崩壊したのは、ブレトンウッズの後継である短命であったスミソニアン協定であり、このことが、変動為替の先駆けとなった。)ドイツの通貨はドルに固定していた。そのことがインフレ圧力となっていることが分かっていた。 ドイツは、その問題は、ドイツマルクを変動制にすることで解決した。その後のことは周知の通り。

Oh, and right now Spain faces deflationary pressure because it can’t devalue, yet the economy wants a depreciated real exchange rate.

今まさにスペインがデフレ圧力に直面している。なぜなら、スペインは通貨の切り下げをできないが、経済は実質為替レートを下げることを求めている。

So China is basically trying to keep water from flowing downhill. And it really needs to stop.

したがって、中国は基本的に坂を流れる水を止めようとしている。 本当に止めるべきだ。

輸出大国である中国の人民元が、不当に低い水準にあることは、クルーグマンは昔からお怒り。

Renminbi RX

中国人民元(RMB = RenminBi 人民幣) RX = EP*/P

Dean Baker is right: it’s bizarre to report that Chinese officials are (a) worried about inflation and (b) determined not to let their currency appreciate without noting that these are contradictory policies.

このリンク先でのディーン・ベイカーの主張は、正しいよ。中国高官はインフレに怯えて、これらは矛盾した政策以外何物でもないのに人民元切り上げを実施しようとしない。

Consider the real exchange rate, defined as RX = EP*/P, where E is the exchange rate measured as the domestic currency price of foreign currency (so an appreciation of the renminbi is a fall in E), P* is the foreign price level, and P the domestic price level. Basic international macro says that there is a “natural” level of the real exchange rate, determined by trade competitiveness and international capital flows. And the economy “wants” to get to that real exchange rate.

為替レートを考慮すると、RX = EP*/Pと定義される。

Eは、国内通貨の海外通貨での価値(人民元の切り上げは、Eの下落になる)

P*は、外国の物価水準

Pは、国内の物価水準

基本的な国際マクロ経済学では、実質為替レートには、市場競争力や国際的な資本の流れによって、適切な水準がある。 経済は、実質為替レートに近づこうとする。

If you have a floating exchange rate, you get there via a rise or fall in E. But if you have a pegged rate, there’s pressure on prices instead. By deliberately keeping E higher than it would be under floating, China is creating pressures for P to rise; the inflationary pressures are directly related to the exchange rate policy.

変動為替相場を採用しているのであれば、E(国内通貨の海外通貨での価値)の上下によって価格が形成される。しかし、固定為替相場であるなら、故意にEを高くすることによって価格に圧力を与えることになる。中国では、P(国内の物価水準)が上がるのを抑えるために価格形成をしている。 つまり、インフレ圧力は、直接為替政策に関係している。

This isn’t a new story. The proximate cause of the breakup of

過去にも事例がある。最も最近の例では、ブレトンウッズ体制の崩壊を引き起こしている。

(正確には、そうではない。崩壊したのは、ブレトンウッズの後継である短命であったスミソニアン協定であり、このことが、変動為替の先駆けとなった。)ドイツの通貨はドルに固定していた。そのことがインフレ圧力となっていることが分かっていた。 ドイツは、その問題は、ドイツマルクを変動制にすることで解決した。その後のことは周知の通り。

Oh, and right now Spain faces deflationary pressure because it can’t devalue, yet the economy wants a depreciated real exchange rate.

今まさにスペインがデフレ圧力に直面している。なぜなら、スペインは通貨の切り下げをできないが、経済は実質為替レートを下げることを求めている。

So China is basically trying to keep water from flowing downhill. And it really needs to stop.

したがって、中国は基本的に坂を流れる水を止めようとしている。 本当に止めるべきだ。

輸出大国である中国の人民元が、不当に低い水準にあることは、クルーグマンは昔からお怒り。

1228 Age of diminished expectations

December 28, 2009, 8:53 am

Age of diminished expectations

期待が減退した時代

“Economy poised for surge as most accurate economist see U.S.” reads the Bloomberg headline. So it’s a major disappointment to read what Bloomberg considers a “surge”: 3.5 percent growth in 2010.

ブルームバーグヘッドラインを読むと、ほとんどの緻密なエコノミスト達がアメリカを見て、経済が急回復する構えを見せていると。ブルームバーグが急回復と見なしているものは、2010年の3.5%の成長率なので、ほんとガッカリするよ。

Um, that’s really subpar for recoveries, let alone recoveries from deep slumps:

それじゃ、本当に景気回復と呼べる代物じゃないよ、長いスランプからちょっと回復しただけだよ。

Or put it this way: during the Clinton years — a 8-year stretch — the average rate of growth was 3.7 percent. Growth at the pace Dean Maki predicts should be enough to bring unemployment down — but not by much. And his prediction is “among the highest” among 58 economists.

もしくは、以下のようにも言うことができる。

クリントン時代の8期では、平均成長率は3.7%であった。 ディエン・マッキ(バークレーズ銀行)の予測する3.5%の成長率で、十分ではないが、失業を抑えることができると。ただ、彼の予測は58人のエコノミストの中だけの話。

I hope he’s right, although my money is still on the more downbeat views of the Goldman guys. Still, it’s amazing how we’ve defined economic success down.

彼の主張が正しいことを祈るよ。ただ、私の資金は、ゴールドマンサックスの主張である景気後退に賭けておくけど・・。けれども、自分たちで経済成長を低く定義し直すなんて、ありえないよ。

Age of diminished expectations

期待が減退した時代

“Economy poised for surge as most accurate economist see U.S.” reads the Bloomberg headline. So it’s a major disappointment to read what Bloomberg considers a “surge”: 3.5 percent growth in 2010.

ブルームバーグヘッドラインを読むと、ほとんどの緻密なエコノミスト達がアメリカを見て、経済が急回復する構えを見せていると。ブルームバーグが急回復と見なしているものは、2010年の3.5%の成長率なので、ほんとガッカリするよ。

Um, that’s really subpar for recoveries, let alone recoveries from deep slumps:

それじゃ、本当に景気回復と呼べる代物じゃないよ、長いスランプからちょっと回復しただけだよ。

Or put it this way: during the Clinton years — a 8-year stretch — the average rate of growth was 3.7 percent. Growth at the pace Dean Maki predicts should be enough to bring unemployment down — but not by much. And his prediction is “among the highest” among 58 economists.

もしくは、以下のようにも言うことができる。

クリントン時代の8期では、平均成長率は3.7%であった。 ディエン・マッキ(バークレーズ銀行)の予測する3.5%の成長率で、十分ではないが、失業を抑えることができると。ただ、彼の予測は58人のエコノミストの中だけの話。

I hope he’s right, although my money is still on the more downbeat views of the Goldman guys. Still, it’s amazing how we’ve defined economic success down.

彼の主張が正しいことを祈るよ。ただ、私の資金は、ゴールドマンサックスの主張である景気後退に賭けておくけど・・。けれども、自分たちで経済成長を低く定義し直すなんて、ありえないよ。

1227 The malleability of history

December 27, 2009, 5:54 pm

The malleability of history

歴史の可塑性(戻れないこと)

Via Atrios, Mary Matalin:

アトリオス、メアリー・マタリン(共和党のコンサルタント)によると

I was there. We inherited a recession from President Clinton and we inherited the most tragic attack on our own soil in our nation’s history. And President Bush dealt with it. And within a year of his presidency at this comparable time, unemployment was at 5 percent. And we were creating jobs.

まだあの当時のままだ。我々は、クリントン大統領の不景気を引き継いでいる。国民国家の歴史において、もっとも悲劇的な病魔を引き継いでいる。 ブッシュ大統領は、それに対処した。そして、これに匹敵する時代において、その任期の1年以内に失業率は5パーセントになった。雇用を作り出したのだ。

Uh, leaving aside the question of who was president on 9/11/01,

ムムム・・ 2009/11/1のテロの時に、大統領であったという疑問を完全に無視している。

↓クルーグマンが用意したチャートでは、ブッシュはグレーの網掛けで911の戦争で、失業率が下がったと言いたいようです。

The malleability of history

歴史の可塑性(戻れないこと)

Via Atrios, Mary Matalin:

アトリオス、メアリー・マタリン(共和党のコンサルタント)によると

I was there. We inherited a recession from President Clinton and we inherited the most tragic attack on our own soil in our nation’s history. And President Bush dealt with it. And within a year of his presidency at this comparable time, unemployment was at 5 percent. And we were creating jobs.

まだあの当時のままだ。我々は、クリントン大統領の不景気を引き継いでいる。国民国家の歴史において、もっとも悲劇的な病魔を引き継いでいる。 ブッシュ大統領は、それに対処した。そして、これに匹敵する時代において、その任期の1年以内に失業率は5パーセントになった。雇用を作り出したのだ。

Uh, leaving aside the question of who was president on 9/11/01,

ムムム・・ 2009/11/1のテロの時に、大統領であったという疑問を完全に無視している。

↓クルーグマンが用意したチャートでは、ブッシュはグレーの網掛けで911の戦争で、失業率が下がったと言いたいようです。

1227 Stimulus timing

December 27, 2009, 5:19 pm

Stimulus timing

経済刺激策のタイミング

One thing that often becomes clear when we talk about prospects for next year — which worry me — is that there’s a lot of confusion over the timing of stimulus impacts. Even well-informed people will say things like “we’ve only spent a quarter of the money, so let’s wait and see what happens.” Menzie Chinn tried to get at this confusion recently; here’s my take.

来年の見通しについて話す時に、ある1つのことがはっきりしている。私も心配していることで、経済刺激策のタイミングでの大混乱である。 情報通の人でさえ、”我々はすでに4分の1の資金を使ったので、どうなるか見守ろう”と言っている。メンジー・チン教授は、最近のこの混乱を解説しようとしていた。 これが、私の見解である。

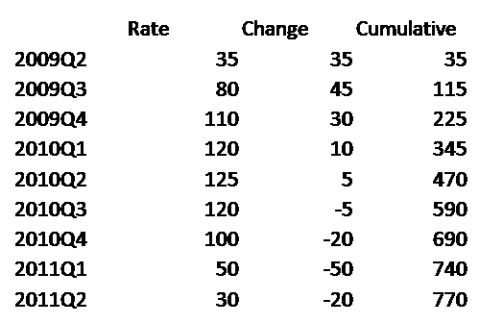

Let me work with a stylized numerical example. It doesn’t quite match the real stimulus — there’s no distinction between spending and tax cuts, and it tails off much faster than the real thing. But I think it’s close enough to make the point. Here’s the table:

図式化された数値データを使って説明させてくれ。実際の経済刺激策とは、全然一致していない。消費と減税との区分けがないので、実際の数値より早く切り捨ててしまっているからだ。ただ、これでも十分私の見解を主張することができる。以下がテーブルである。

In the table, “Rate” is the total stimulus spending within each quarter. “Change” is the change in stimulus spending from the previous quarter. And “Cumulative is the total spending to date.

“Rate” その四半期の中での経済刺激策の総消費値。

“Change” 前四半期からの経済刺激策の消費量の変化値。

“Cumulative ” 総消費値。

Now think about three questions you might ask. The first is, how much higher is GDP this quarter than it would be without the stimulus? This should depend on “Rate” — on the quantity of goods and services the government is buying right now.

今、質問されるだろう3つのことが思い浮かぶ。

まず第1に、経済刺激策がなかったら、今四半期はGDPはどれほどだろうか?

これは政府が現在購入している商品とサービスの数値である、“Rate”から推測できる。

The second question is, how much faster is GDP growth this quarter than it would be without the stimulus? This should depend on “Change” — on the extent to which the government is buying more stuff than it did last quarter.

第2の質問は、経済刺激策がなかったら、今四半期のGDP成長率ははどれほどだろうか?

これは政府が前四半期に購入してから、今期購入しているモノの数値である、“Change”から推測できる。

Finally, you can ask, how much of the stimulus money has been spent? For that you want to look at “Cumulative”, and compare it with the final total for that column.

最後の質問は、経済刺激策はお金をどこまで使っているのか?

“Cumulative”をみれば分かる。 このコラムで、現時点の総額と最終総額を比較しておく。

Now the point is that “Rate”, in real life, follows an inverted U. The peak effect on the level of GDP comes at the top of the curve, but the peak effect on growth comes earlier, before the curve flattens out. In the table above, spending peaks in the second quarter of 2010, but the peak impact on growth is in the third quarter of 2009, i.e., it’s behind us. That’s true even though by the end of 2009 less than a third of the money has been spent.

実生活では、“Rate”(消費量)は、逆U字型になることが重要である。そのピークは、GDPがカーブの頂点に達する時期に影響するが、カーブが平らになる前に、そのGDP成長のピークは過ぎてしまった。上のテーブルでは、経済刺激策の消費ピークは、2010年第2四半期になっているが、そのGDP成長へのインパクトは、2009年の第3四半期である。つまり、もう過ぎてしまったということだ。

また、2009年第3四半期までに資金の3分の1は、使い果たしてしまったことも事実である。

And when the spending begins to tail off, the effect on growth turns negative.

経済刺激策が尽きたら、GDP成長への効果は後退するだろう。

What does this really look like? Menzie gives us the chart from Deutsche Bank, which is similar to other estimates, e.g. from Goldman Sachs:

このことを本当にどう思う? ドイツバンクのリサーチによるチャートでも指し示している。

同じような予測は、例えばゴールドマン・サックスなどでもしている。

You can see why I and many others are worried about the second half of next year.

なぜ、私も含め多くの人が来年の後半を心配しているか分かるでしょ。

Stimulus timing

経済刺激策のタイミング

One thing that often becomes clear when we talk about prospects for next year — which worry me — is that there’s a lot of confusion over the timing of stimulus impacts. Even well-informed people will say things like “we’ve only spent a quarter of the money, so let’s wait and see what happens.” Menzie Chinn tried to get at this confusion recently; here’s my take.

来年の見通しについて話す時に、ある1つのことがはっきりしている。私も心配していることで、経済刺激策のタイミングでの大混乱である。 情報通の人でさえ、”我々はすでに4分の1の資金を使ったので、どうなるか見守ろう”と言っている。メンジー・チン教授は、最近のこの混乱を解説しようとしていた。 これが、私の見解である。

Let me work with a stylized numerical example. It doesn’t quite match the real stimulus — there’s no distinction between spending and tax cuts, and it tails off much faster than the real thing. But I think it’s close enough to make the point. Here’s the table:

図式化された数値データを使って説明させてくれ。実際の経済刺激策とは、全然一致していない。消費と減税との区分けがないので、実際の数値より早く切り捨ててしまっているからだ。ただ、これでも十分私の見解を主張することができる。以下がテーブルである。

In the table, “Rate” is the total stimulus spending within each quarter. “Change” is the change in stimulus spending from the previous quarter. And “Cumulative is the total spending to date.

“Rate” その四半期の中での経済刺激策の総消費値。

“Change” 前四半期からの経済刺激策の消費量の変化値。

“Cumulative ” 総消費値。

Now think about three questions you might ask. The first is, how much higher is GDP this quarter than it would be without the stimulus? This should depend on “Rate” — on the quantity of goods and services the government is buying right now.

今、質問されるだろう3つのことが思い浮かぶ。

まず第1に、経済刺激策がなかったら、今四半期はGDPはどれほどだろうか?

これは政府が現在購入している商品とサービスの数値である、“Rate”から推測できる。

The second question is, how much faster is GDP growth this quarter than it would be without the stimulus? This should depend on “Change” — on the extent to which the government is buying more stuff than it did last quarter.

第2の質問は、経済刺激策がなかったら、今四半期のGDP成長率ははどれほどだろうか?

これは政府が前四半期に購入してから、今期購入しているモノの数値である、“Change”から推測できる。

Finally, you can ask, how much of the stimulus money has been spent? For that you want to look at “Cumulative”, and compare it with the final total for that column.

最後の質問は、経済刺激策はお金をどこまで使っているのか?

“Cumulative”をみれば分かる。 このコラムで、現時点の総額と最終総額を比較しておく。

Now the point is that “Rate”, in real life, follows an inverted U. The peak effect on the level of GDP comes at the top of the curve, but the peak effect on growth comes earlier, before the curve flattens out. In the table above, spending peaks in the second quarter of 2010, but the peak impact on growth is in the third quarter of 2009, i.e., it’s behind us. That’s true even though by the end of 2009 less than a third of the money has been spent.

実生活では、“Rate”(消費量)は、逆U字型になることが重要である。そのピークは、GDPがカーブの頂点に達する時期に影響するが、カーブが平らになる前に、そのGDP成長のピークは過ぎてしまった。上のテーブルでは、経済刺激策の消費ピークは、2010年第2四半期になっているが、そのGDP成長へのインパクトは、2009年の第3四半期である。つまり、もう過ぎてしまったということだ。

また、2009年第3四半期までに資金の3分の1は、使い果たしてしまったことも事実である。

And when the spending begins to tail off, the effect on growth turns negative.

経済刺激策が尽きたら、GDP成長への効果は後退するだろう。

What does this really look like? Menzie gives us the chart from Deutsche Bank, which is similar to other estimates, e.g. from Goldman Sachs:

このことを本当にどう思う? ドイツバンクのリサーチによるチャートでも指し示している。

同じような予測は、例えばゴールドマン・サックスなどでもしている。

You can see why I and many others are worried about the second half of next year.

なぜ、私も含め多くの人が来年の後半を心配しているか分かるでしょ。

1224 Noo Yawk Roolz!

December 24, 2009, 10:47 am

Noo Yawk Roolz!

ヌーヨーク最高!!(ニューヨーク訛り)

I watched the Senate vote this morning, and despite all, it was an inspiring moment. A few random thoughts:

今朝、上院投票を見ていた。 全てではないが、刺激的な瞬間だった。いくつか手当たりしだいの考えを並べた。

1. It’s petty and silly, but after what seems like a whole adult lifetime in which Central Casting insisted that major politicians be either Southern gentlemen or Midwestern heartland types, it felt good to watch and listen to Chuck Schumer, speaking the language of my roots, at the victory press conference — even with that green tie. Noo Yawk Roolz!

1.ちっぽけでバカげたことだが、セントラル・キャスティング(俳優学校)では、大物政治家役は南部紳士タイプか中西部ハートランド紳士のどちらか一方であると言われ続けた半生であった。

(つまり東部の東欧系ユダヤ人であることがイメージと合わないと)

そのチュック・シューマー上院議員が、私の故郷の言葉[であるニューヨーク訛り]で勝利宣言をする記者会見を目と耳で感じ取れたのは嬉しかった。ヌー・ヨーク最高!!ただ、あの緑のネクタイもどうかと思ったが・・・

2. More seriously, Jon Chait is right: this is a great achievement.

2.真面目な話をすると、Jon Chait は正しい。これは偉業である。

3. As expected, self-proclaimed centrists can’t bring themselves to say anything nice about a bill that delivers everything they claim to want. Many people have pointed to David Broder’s piece this morning; let me add a historical note. Back in 2006, Broder hailed the Massachusetts health reform as a “major policy success”. Now the Senate has passed a bill that is, broadly speaking, a better-funded version of the MA plan plus a major effort at cost control. Where’s the praise?

3.期待していたとおりに、自称セントリス達は、自分たちが希望した法案について何も世論の支持をえることができないでいる。今朝、多くの人がワシントン・ポストのベテラン・コラムニストDavid Broderの記事に指摘している。 歴史的な注釈を付けると、2006年にBroderは、マサチュセッツの医療法案を大成功として称賛していた。

http://www.washingtonpost.com/wp-dyn/content/article/2006/11/25/AR2006112500736.html

たった今、上院が通過させた法案は、マサチュセッツの法案にコスト面でより優れているバージョンである。称賛じゃないのか?

Anyway, a pretty good morning.

いずれにせよ、心地良い朝だ。

法案通過 クルーグマンおめでとう。

Noo Yawk Roolz!

ヌーヨーク最高!!(ニューヨーク訛り)

I watched the Senate vote this morning, and despite all, it was an inspiring moment. A few random thoughts:

今朝、上院投票を見ていた。 全てではないが、刺激的な瞬間だった。いくつか手当たりしだいの考えを並べた。

1. It’s petty and silly, but after what seems like a whole adult lifetime in which Central Casting insisted that major politicians be either Southern gentlemen or Midwestern heartland types, it felt good to watch and listen to Chuck Schumer, speaking the language of my roots, at the victory press conference — even with that green tie. Noo Yawk Roolz!

1.ちっぽけでバカげたことだが、セントラル・キャスティング(俳優学校)では、大物政治家役は南部紳士タイプか中西部ハートランド紳士のどちらか一方であると言われ続けた半生であった。

(つまり東部の東欧系ユダヤ人であることがイメージと合わないと)

そのチュック・シューマー上院議員が、私の故郷の言葉[であるニューヨーク訛り]で勝利宣言をする記者会見を目と耳で感じ取れたのは嬉しかった。ヌー・ヨーク最高!!ただ、あの緑のネクタイもどうかと思ったが・・・

2. More seriously, Jon Chait is right: this is a great achievement.

2.真面目な話をすると、Jon Chait は正しい。これは偉業である。

3. As expected, self-proclaimed centrists can’t bring themselves to say anything nice about a bill that delivers everything they claim to want. Many people have pointed to David Broder’s piece this morning; let me add a historical note. Back in 2006, Broder hailed the Massachusetts health reform as a “major policy success”. Now the Senate has passed a bill that is, broadly speaking, a better-funded version of the MA plan plus a major effort at cost control. Where’s the praise?

3.期待していたとおりに、自称セントリス達は、自分たちが希望した法案について何も世論の支持をえることができないでいる。今朝、多くの人がワシントン・ポストのベテラン・コラムニストDavid Broderの記事に指摘している。 歴史的な注釈を付けると、2006年にBroderは、マサチュセッツの医療法案を大成功として称賛していた。

http://www.washingtonpost.com/wp-dyn/content/article/2006/11/25/AR2006112500736.html

たった今、上院が通過させた法案は、マサチュセッツの法案にコスト面でより優れているバージョンである。称賛じゃないのか?

Anyway, a pretty good morning.

いずれにせよ、心地良い朝だ。

法案通過 クルーグマンおめでとう。

登録:

投稿 (Atom)